Guest Post by Milena Dehn, 2024-2025 Sustainability Leadership Fellow and Ph.D. Student in the Department of Economics at Colorado State University

Global sovereign debt burdens have followed a concerning trend in recent years. After a period of decline since the 1980s, both public debt levels and debt servicing costs have been increasing steadily since 2010. In many countries across the Global South, debt service payments now far exceed investments in climate change mitigation and adaptation – at a time when climate finance is more urgently needed than ever.

Notes. Own figure. Debt refers to external public and publicly guaranteed debt stock (% of GDP). Debt service are external public and publicly guaranteed debt service payments (% of exports). Median of country group. Source: IMF IDS and World Bank WDI.

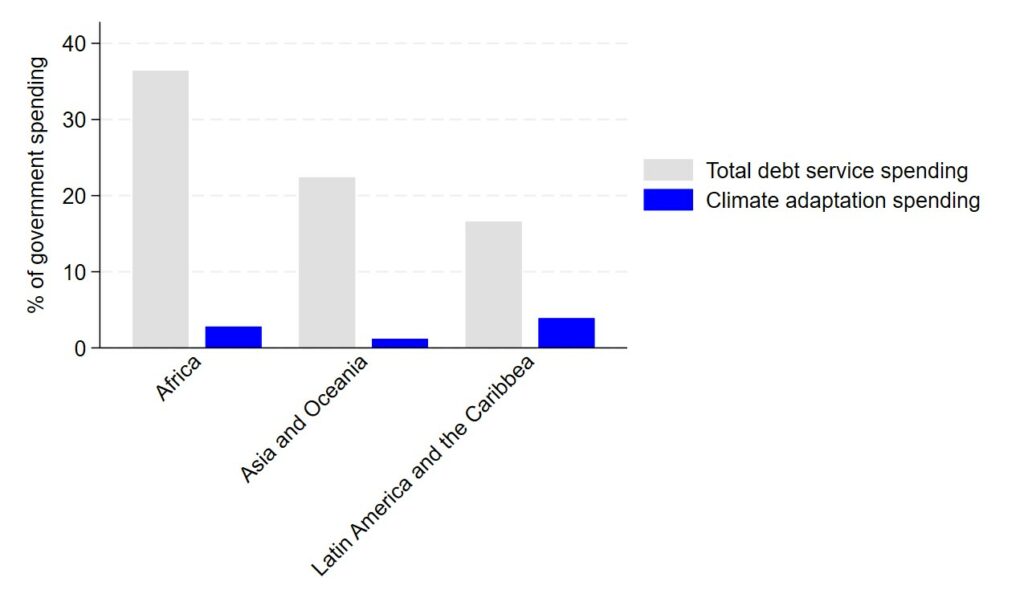

The problem of high debt burdens is that they imply high debt servicing costs: countries have to use a significant amount of their government budget to pay back the debt principal and interest payments. This limits their ability to invest in other areas. In recent years, there is a growing number of developing countries that spend a higher proportion of the government budget on debt servicing than on education, health or climate change adaptation (Figure 2).

Notes. Figure based on DFI (2023) and data collected by Development Finance International and Debt Justice. Data based on 42 developing countries.

It is evident then that many countries of the Global South have very little scope to scale up spending on climate change mitigation and adaptation. The double bind of the debt and climate crises shows that it is time to address both together. And one tool that has gained attention in this debate is the debt-for-nature swap. Debt-for-nature swaps reduce a country’s debt burden while ensuring that foregone debt service payments are directed toward environmental protection efforts. Several studies indicate the high potential of this tool in addressing climate change, but it is too early to evaluate actual implementations. However, debt-for-nature swaps are not a new tool and it seems worthwhile to revisit how this tool has been used to tackle the debt crisis and increasing deforestation in the 1980s.

Indeed, it is not the first time a debt crisis and growing concern for the environment have hit at the same time. In the 1970s, many Latin American countries took on significant debt for development projects, but the early 1980s recession and falling oil prices caused export revenues to decline, making it harder to service external debt. This economic situation also put mounting pressure on tropical forests. The reason is that debt service payments must often be paid in US dollars rather than local currencies. To meet these payments, affected countries ramped up agricultural, timber, and mining exports to generate foreign exchange – all activities that contribute to deforestation. This pattern was exacerbated by the structural adjustment programs introduced by the International Monetary Fund and the World Bank. These programs, designed to stabilize economies and secure debt relief, often prioritized export-oriented growth and encouraged a focus on export crops, ultimately increasing deforestation (Culas 2006).

In response to the dual crisis of debt and deforestation, Thomas Lovejoy of the World Wildlife Fund introduced the concept of debt-for-nature swaps. The aim is to simultaneously address economic and ecological challenges by cancelling parts of sovereign debt and converting debt service payments into conservation funding. In a typical arrangement, a creditor country or NGO purchases a portion of a developing country’s outstanding debt under the condition that a portion of the repayment – now in local currency – is redirected to finance conservation projects within the debtor nation.

Debt-for-nature swaps have by now been implemented in more than 30 countries – but their impact remains contested. While they generate funds earmarked for forest conservation, some case studies indicate that projects led to the displacement of local communities or that swaps merely replaced funding from other sources. Besides, the effectiveness of the swaps in reducing export dependency and restoring the spending capacity of governments depends on the debt relief being sufficiently high – and most assessments of past swaps imply that this was not the case. Additionally, conditional debt relief has been criticized as a form of neo-colonialism, since the conditionalities prioritize foreign interests and often bypass local structures. Despite these criticisms, debt-for-nature swaps have been defended as a pragmatic tool for generating at least some conservation funding and canceling at least some magnitude of sovereign debt. Since debtors continue to make payments – now redirected toward environmental projects – debt-for-nature swaps might also help to convince creditors who are critical of unconditional debt cancellation. And compared to debt-for-resource swaps, the generated funds are invested locally (Cassimon et al. 2011, Essers et al. 2021, Culas 2006).

In any case, the emerging debt crisis and the urgent need to tackle climate change have led to renewed interest in debt-for-nature swaps and reports such as Volz et al. (2020) explicitly discuss the potential of debt-for-climate swaps. While the experiences of debt-for-nature swaps focused on deforestation offer only partial guidance, they illustrate the potential of tackling economic and environmental crises jointly. However, past experiences also show that it is relevant that debt reduction levels are sufficiently high, and that debt relief is implemented quickly and without restricting the sovereignty of local communities and governments. Volz et al. (2020) thus stress that any piecemeal solution and lengthy negotiations of individual swaps will not suffice. Instead, debt-for-climate swaps have to be implemented as part of a concerted and comprehensive debt relief initiative that includes the commitment to use some of the new spending capacity for climate change mitigation and adaptation.

References

Cassimon D, Prowse M and Dennis Essers (2011). The pitfalls and potential of debt-for-nature swaps: A US-Indonesia case study. Glob Environ Change 21:93–102.

Culas, R J (2006). Debt and Deforestation: A Review of Causes and Empirical Evidence. Journal of Developing Societies, 22: 4, 347-358.

DFI (2023) The worst ever global debt crisis: putting climate adaptation spending out of reach. Debt Service Watch Briefing 2023 by Development Finance International.

Essers, D., Cassimon, D. & Prowse, M. (2021). Debt-for-climate swaps: killing two birds with one stone? Global Environmental Change, 71, 102-407.

Volz, U., Akhtar, S., Gallagher, K. P., Griffith-Jones, S., & Haas, J. (2020). Debt relief for a green and inclusive recovery. Heinrich Böll Foundation, the Center for Sustainable Finance at SOAS, University of London, Boston University Global Development Policy Center.